Key Take Aways from Northern New Jersey’s March 2022 Meeting

- John Tregidgo (Dresdner Robin) opened the meeting with a reference to current world events driving more volatility in the market – inflation is up and both supply chain and cyber security issues continue to increase. In the NJ residential market, rent rates continue to rise. He reported that the NJ DEP is nearing the end of its remedial action phase on many projects that have been stalled for various reasons. This presents an opportunity for property owners to handle remediations for possible sales in the future.

- Charles Heydt (Dresdner Robin) noted that a lot of environmental applications are being submitted electronically, a faster and more efficient process than in-person meetings. However, much detail is potentially lost — a downside for project planning, especially on larger projects. He is still seeing a lot of multifamily/mixed use/urban infill projects that require education with smaller or first-time developers.

- Tony Ianuale (Dresdner Robin) added that Dresdner Robin’s YOY new business activity was up 10% over 2021, with residential and industrial projects still in high demand, even without the pending infrastructure money disbursement from the government.

- Greg James (NAI James Hanson) reported that the biggest change in the financial market is due to the war in Ukraine. The yield curve has flattened since early December, and we are in for some volatility over the next 2-3 months. There is a 25 to 30% chance of a recession in the 4th quarter or early next year.

- Paul Hacker (Axis Insurance) noted that even before the war in Ukraine insurance costs in all categories had increased and will continue to do so over the next year or two. Cyber breaches and insurance premiums are expected to increase, with potential liability for shareholders. Even before the war, many carriers had reached their capacity for cyber insurance, even when requiring anti-cyber protocols be in place. Experts anticipate increased Russian hacking in critical infrastructure sectors, especially energy.

- Art Makris (Duke Realty) provided an overview of his firm, focusing on its Construction segment in five coastal markets (NJ/PA/mid-Atlantic, SoCA, NoCA, Seattle, and Miami). They’ve grown the NJ/PA market from zero to $4B investment capital and are geared up to do $300M in construction sales annually. Construction projects in NJ and PA are currently at more than $400M. He noted that commodity pricing is increasing after leveling off pre-war. Roofers are no longer locking in pricing; by the end of March, there will be no pricing guarantees until items are shipped.

- Richard Miller (Pegasus Group) described his firm’s focus as the development and redevelopment of “logistically challenged” assets in urban markets, notably upscale multifamily/mixed use properties. Between 2010-2020, Pegasus transformed Harrison, making it the fastest growing town by 40%. For example, they partnered with Iron State to develop land near Harrison PATH station — 1900 apartments with a 180-room hotel and 30K SF retail. Another current project: the Harrison Urby mixed use project currently has 384 upscale apartments with 500 parking spaces and 3,760 SF of retail, including a new German restaurant.

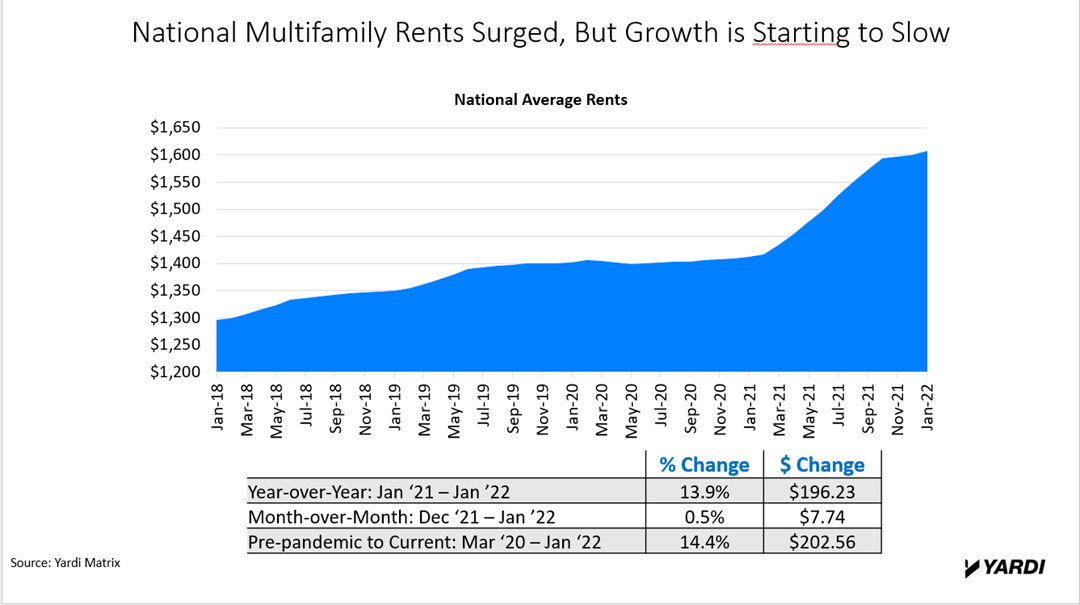

- Speaker Paul Fiorilla (Yardi Systems) summarized the state of the multifamily nationally.

- Multi-family had the highest rent growth in decades, with 600K units absorbed (the biggest number seen in decades). Gateway and secondary markets bounced back by 4.9%; tertiary markets not as strong; the northeast market was at a healthy 3.6%.

- Pent-up demand for multifamily coming out of the pandemic, with 6M jobs created and the economy recovering. Young people have income and are choosing to rent; Boomers/retirees are downsizing to rentals – increasing the demand for high-profile rental units. There is a higher trend in lifestyle vs. rent by necessity.

- 872K rental units are under construction nationally; 51,557 units are planned for Northern NJ. With demand still high, prices are surging.

- 2021 migration patterns have continued, with more people leaving major gateway markets for less expensive SE and SW sunbelt markets, fueled by cost of living and ease of work-at-home from anywhere options.

Recent Comments