Pittsburgh August 2022 – Key Take-Aways

Mekael Teshome, Federal Reserve Bank

- Real GDP declined by almost a percentage point in the first half of the year. Consumer spending was a net positive in the second quarter, but its contribution to growth has diminished, relative to 2021. According to Blue Chip forecasters, we could be at 1.5 percent real GDP growth for the full year 2022, and little more than a 0.5 percent in 2023.

- In the Pittsburgh region, activity also softened. In responses to a Pennsylvania Economy League survey, businesses reported weaker activity. The July survey still had a net positive share of firms seeing growth, but those shares clearly have diminished since 2021.

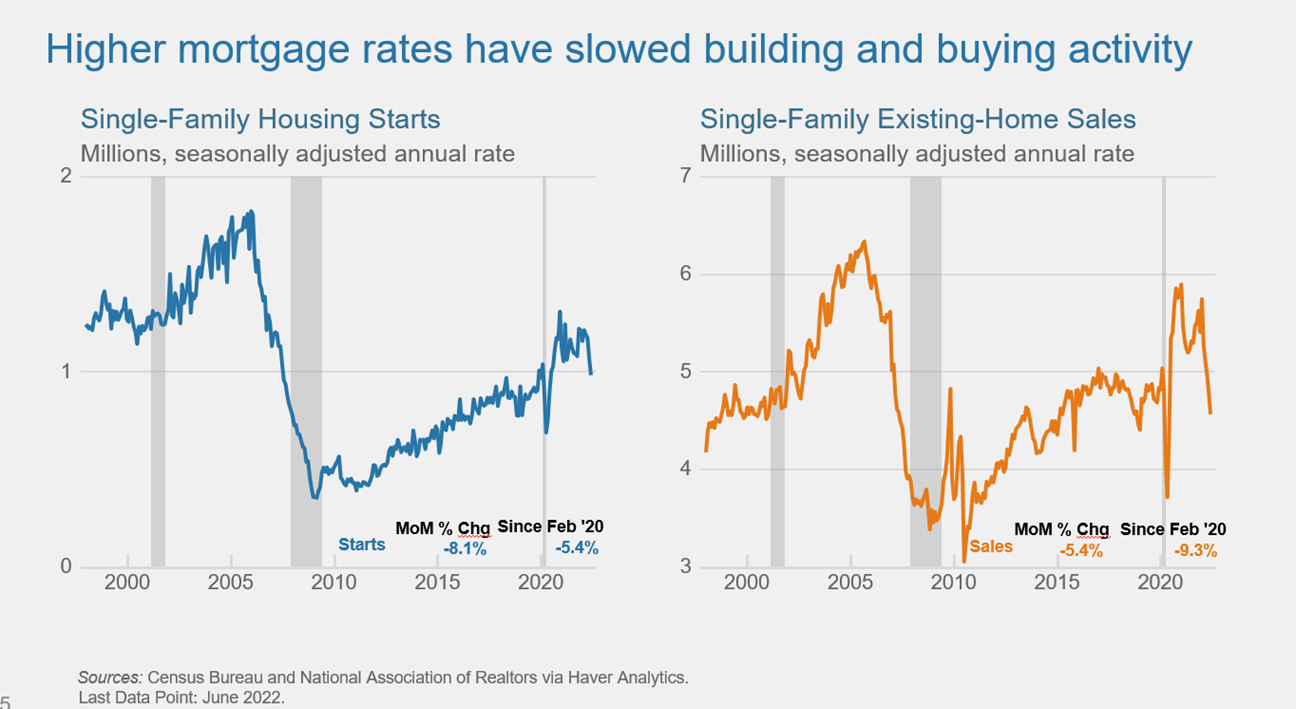

- Monthly, we’re seeing the impact of higher interest rates affecting activity – it’s most noticeable in housing. Building has slowed. The nonresidential side has lost some momentum as well, but not like the housing sector. Industrial production and manufacturing are also weaker — it’s really a broad-based slowdown in manufacturing.

- Consumer spending: Once adjusted for inflation, consumer spending is trending sideways. People are spending on services but cutting back on durable and nondurable goods.

- Companies are recalibrating investment plans. A chamber of commerce says there is hesitation to invest. One said investing in what’s necessary; the phrase “tapping on the brakes” is coming up frequently in conversations. There are concerns about the outlook leading to a downshift in investing, a trimming of inventory.

- Unemployment: Took only a little more than two years to recover. There was a quick recovery but the downside is, labor force participation remains below the pre-pandemic level. We’re not going back to the pre-pandemic level. The consensus view is, participation will remain low for the foreseeable future, unless there’s a policy change.

- Wages continue to rise, and that’s a big part of inflation, so inflation will remain uncomfortably high through the end of next year.

Jennefer Bartholomew, UBS – Speaking about commodities, we’re in a midterm election year so the market has responded accordingly, and we’ll continue to see an upward trend through the election and then it will come back down as the recession conversation still looms. In precious metals, some clients jumped in against sage advice and they’ve ticked down as the market comes back up. We’re staying in some higher growth positions at this point, that we had switched people out of earlier this year; we will continue to reallocate portfolios. We’re monitoring; going to recoup some losses we had earlier this year.

Perry Ninness, UBS – We saw the tax sector comeback in July, after it got creamed. Some super heavy funds were 27 percent down; it’s crawling back, now at 18 percent. We picked up $1 million in net new business in CD rates. Clients coming out of woodwork to park money for 6 months.

John Watt, Valbridge Property Advisors – The upper end of the new home market remains strong and is pretty positive; there’s a backlog of homes sold but not constructed, and we’re not seeing a lot of people back out. On the lower side, people are being hit harder with the cost of gas and the cost of financing mortgages. So, we’ve chopped the bottom quarter to third of the buying market out of the market. There’s industrial change along the Ohio River, from Huntington up through Wheeling to the cracker plant; coal and gasification plants in Mason County. Long-term gas and coal use will continue; we’ll be using coal for the next 20 or 30 years, just not at the rate we have.

Ray Steeb, Efacility LLC – Inflation pressure hasn’t gotten down to facility maintenance personnel and labor-specific construction personnel, and when it does, everyone will want to be more efficient. That’s when we’ll see it go up. People who aren’t going back to work, whether they’ve retired or because they have better opportunities not to go back to their former profession, until more people get into the marketplace, the upper pressure in cost will make things difficult.

Todd Pifer, AdVenture Development LLC – We don’t have too much happening on the Pittsburgh front. We’re still working on McCandless Square, but all our real efforts and direction are in Raleigh, N.C., where we have the big food hall that will be opening on Aug. 26. I’ll be flying down in the next day or so. It will be the first one on an interstate, and not in an urban setting. We have 10 food stations — 8 hooded and two non — so basically, we’re opening 10 restaurants on the same day.

Jim Futrell, Allegheny Conference on Community Development – Our business division is full speed ahead – we have a robust project load, even a couple of call centers. Business investments might be trailing off, but they’re still looking for new facilities.

Gene Boyer, Burns Scalo Real Estate – Mekael’s labor report hit on the core element of what drives Burns Scalo: Highly skilled workers are hard to find and retain. Create high-quality, highly-amenitized office space that makes top talent want to come to the office. Covid is an accelerator: we see a massive bifurcation of old to new. We do not see conversions as a viable strategy except in rare cases. At $300+ / sq. ft. in current construction pricing conditions, Pittsburgh simply will not support those rents in an old, repositioned building. No matter how well it is restored. We are bullish on ground-up new development. Highly amenitized and built for the employees of the future. Also, we are large-scale programmatic developers so it is rare that we would do a small-footprint, one-off development. We remain bullish in the acquisition space for the right property. We would likely never undertake a B or C to A repositioning.

Recent Comments